The Changing Face Of The Taxi Industry

Rickshaw, uber, ola, rapido-

These are all just synonyms synonymous to ‘life saver’ for college students.

Now, imagine if all the rickshaws go on a strike indefinitely…

Well, this has actually happened. Starting December 12th, 16 auto unions in Pune have decided to go on a strike indefinitely in protest of bike taxis (rapido) that are expected to impact the cab aggregator business (Ola and Uber) and have already adversely impacted the income of many rickshawalas . Their demands are – banning bike taxis in the state (interestingly, bike taxis are banned in Karnataka and Assam), cutting CNG prices (or increasing base fare), changing the base policy of electric vehicles (e-vehicles don’t require permits and can roam anywhere in the city- thus, affecting autowalas) and stopping harassment from the finance companies (most auto drivers default on loans because their incomes fluctuate daily and lack stability).

The strike seems to be an attempt to prevent other players from entering the market- a classic monopolist move. So, as the Economics section in our newsletter, we decided to explore the cab aggregator market further which has seen huge ups and downs in the past years.

But first, let’s bust some jargon-

The Ministry of Road Transport and Highways defines cab aggregators as a digital intermediary or market place for the passenger to connect with a driver for the purpose of the transportation. Ola, Uber and other aggregators do not own taxis and rickshaws, instead they provide trips to drivers (who own the vehicle) in exchange for a commission. Such firms bridge the gap between passengers and drivers by providing an app that connects them on demand.

Mega cabs was one of the first cab aggregators launched in India in 2002. It has a B2B (Business to Business- exchange of products, services or information between businesses) model and did not have much of an effect on the taxi sector. Firms like Meru cabs, easy cabs and savaari launched with the same business model but hardly had any market control. All of this changed with the introduction of Ola in late 2010 which had a B2C (Business to consumer) model which sent shockwaves in the taxi industry. It became an instant hit and slowly began to dominate the cab aggregator market in the country.

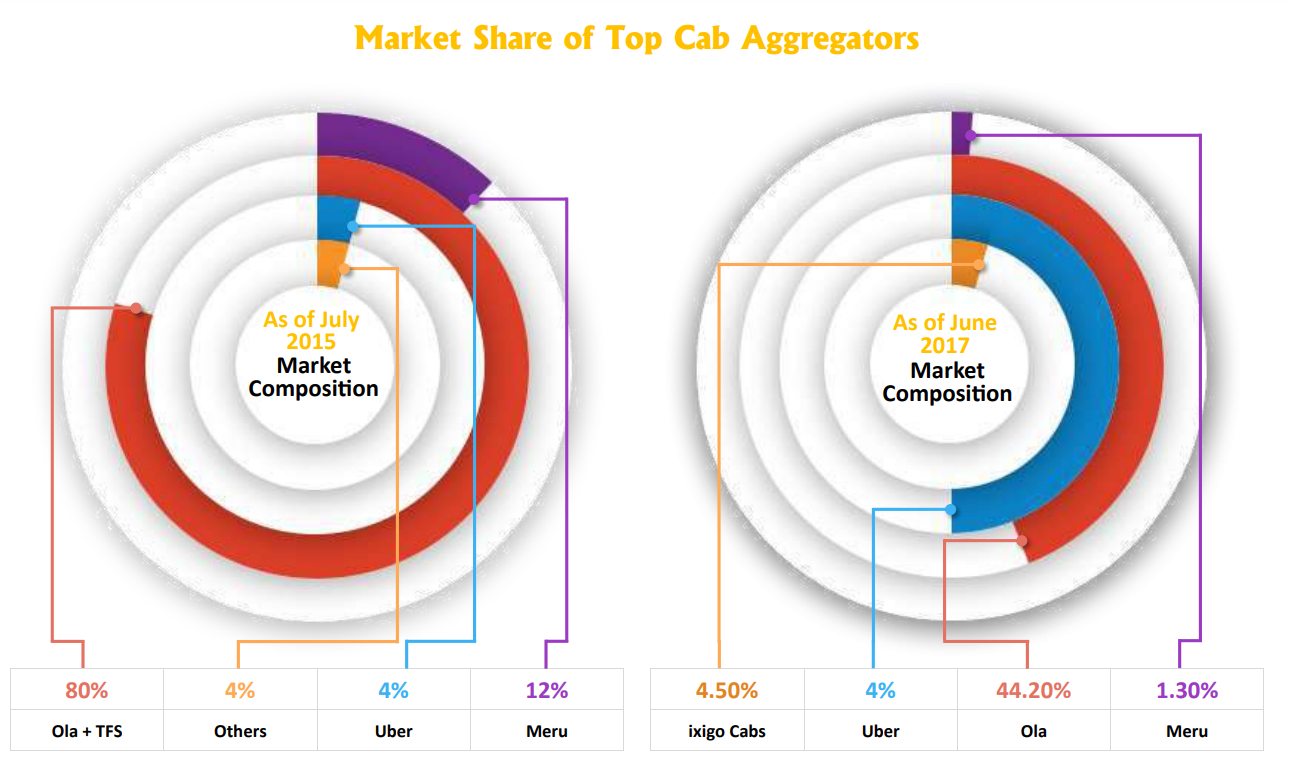

Market share of Cab Aggregators in the early years

From raising $500k in 2011 to becoming a unicorn (valuation of $1 billion) in 2015, Ola was breaking all sorts of records at a great speed. Ola also acquired its main competitor TaxiForSure in 2015 for 12.37 billion rupees ensuring that it controlled most of the market (Uber had just entered the scene in 2013 and was in its nascent stage). This meant that the cab aggregator market showed no signs of becoming a monopolistic competition where many firms could compete against each other with almost equal market shares. Instead, it became a duopoly where two firms, Ola and Uber, controlled most of the market (90 – 95%) and did not have much competition except for each other.

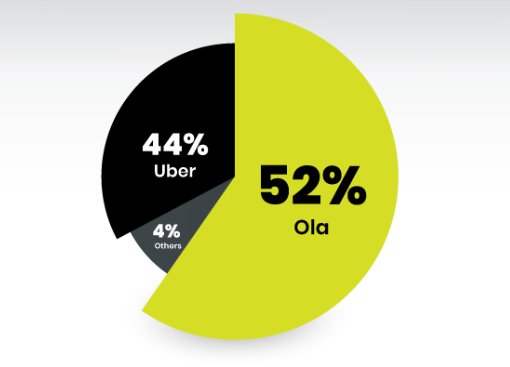

While Ola was the desi startup enjoying its monopoly in the early years, the introduction of the multinational company ‘Uber’ in India in 2013 became the source for its major competition. Around this time, Uber caught up with Ola and the market structure shifted to a competitive duopoly. The price war between the two companies was fierce. Uber had considerably lower rates and better service. However, Uber only operated in around 40 cities (focusing on metro cities). Thus the gap between Uber and Ola’s market share was decreasing everyday.

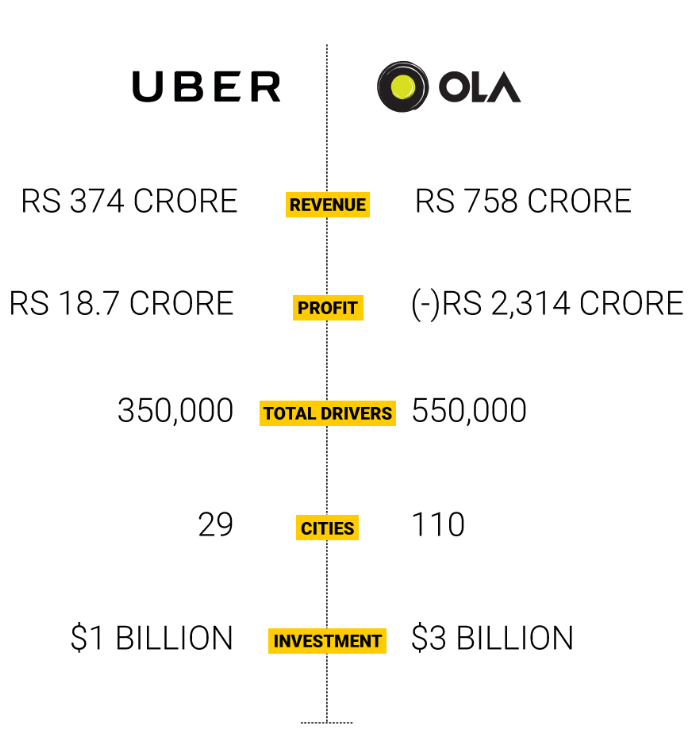

By 2017, the cab aggregator market was booming with about 2 million cab rides everyday in India. Ola claimed that in 2018-19 it had provided 1.5 billion rides and was expecting this number to grow by at least 15% in the next year.

By 2019 Uber claimed to have done about 14 million rides a week whereas its competitor Ola had done about 28 million rides a week.

The cab aggregator market was growing exponentially every year until in 2020 when everything came to a standstill because of the pandemic.

In March 2020, the average profits of most cab aggregators fell by 59%. Driver earnings were near ‘0’ in the lockdown months of April and May. This pushed down the growth of Ola and Uber for 2 years but as of today, business is almost back to pre-lockdown levels.

In 2021, Uber India unlocked an estimated Rs 446 billion in economic value for the Indian economy with its on-demand service for riders, drivers, and the wider community.

The market is expected to reach around 14 billion by the end of 2022 due to the increase in the urban middle class in most cities. It is also inching towards an oligopoly where firms like Meru, Easy Cabs and Jugnoo are reclaiming their market share.

Now if 14 billion seems like a huge number to you, you will be surprised to know that this number is a mere 4-5% of the transport market in India today. 90% of this market is still run by the independent rickshaws and taxis that are run by the metre and auto unions in every city. Thus even though cab aggregators like Ola and Uber have increased their business and profits, the market share for commuters is dominated by the unorganised taxi sector. This statistic shows how badly most commuters will be affected by the indefinite auto union strike. The cab aggregator market will continue to grow but it will be no threat to auto unions for at least another 5 years. This should get you thinking as an economist- What is better in the near future- More cab aggregators entering the scene? Or, More regulations and permits on firms to ensure that the unorganised taxi system doesn’t die?

-Gaargi Jamkar

FY BS.c